Is Oil Going To Top or What?!

- Chris Kline

- Apr 29

- 3 min read

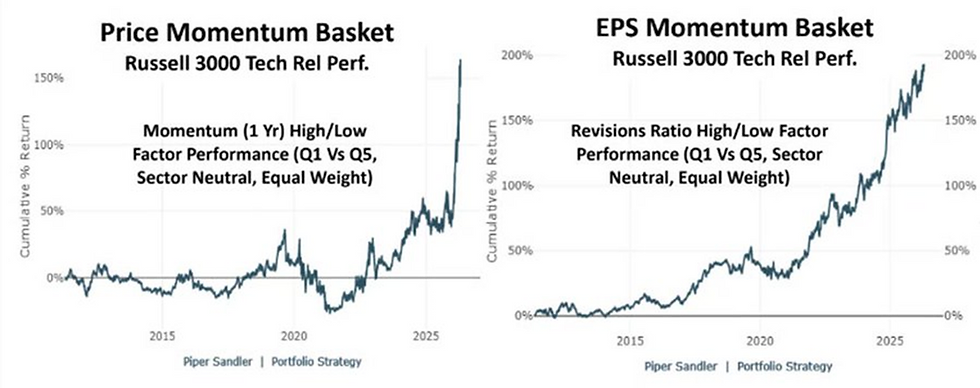

1.) EARNINGS – It’s earnings season, and at the risk of “boring” you with too much earnings data, the data is signaling an important element. 12-month S&P 500 earnings estimates are up an incredible +10% YTD, with 6.5% coming since the war started. The S&P 500 is up +3.79% (through yesterday), but…and this is the important element…they are cheaper now than at the start of the year. On top of that, stocks where earnings are doing the heavy lifting have performed far better over time, with less volatility and smaller drawdowns. Price momentum, driven by EPS momentum, is the best of all momentums!

2.) PASSIVE – A lot of people still believe in this idea of “passive investing.” The story is that you just buy a fund, “set it and forget it.” No decisions. No stock picking. No involvement. But that’s not how this works. All you’re doing is handing the decisions to someone else. The activity doesn’t disappear; it just gets outsourced. And if you’re a “Boglehead” indexer, you’re ignoring the importance of risk management. Drawdown control! Remember the -55% drop in 2008?! Yeah, that can be dangerous. For example, look at the Dow. In 2020, after more than 90 years, they removed Exxon Mobil (XOM) and replaced it with Salesforce (CRM). That wasn’t “passive.” That was an active decision made by the index… if you owned a Dow fund, you had no choice. They chose to take out one of only two energy names in the index right as energy was getting going, and they replaced it with a software stock? As you can see… not great timing. So, index investing is great. But to ignore drawdown control is a dangerous game.

3.) OIL – Well, so far, I’ve been wrong about Oil “topping” in April. It could touch $111 and still put in a lower high that could usher in that top. But signal-wise, it sadly looks like it could go higher in the near term. What could change this? Of course, an end to the Iran war. One interesting element of the war is that Iran's crude output is roughly 3-3.2 million barrels per day (bpd) recently, which is down slightly month-to-month in some data and below historical peaks. But the blockade is restricting exports. So where’s all that oil going? The excess oil Iran is producing but can't export is primarily building up in storage—both onshore tanks and floating tankers—while the country takes desperate measures to create more space. That sounds like a traditional econ 101 issue…lots of supply, neutral demand = pressure on price. Now, at some point, Iran will be forced to limit production since they have nowhere to go with the oil. In the oil business, prolonged shutdowns can damage reservoirs (e.g., water intrusion, pressure loss), leading to irreversible long-term output losses (hundreds of thousands of bpd). And that may in fact be the ultimate objective…permanently damage their economic abilities. Right now, the unsold oil is clogging Iran's storage system, forcing creative (and suboptimal) workarounds while production ramps down. Let’s see if WTI can put in a lower high in the next several days. If so, that “top” might still be in play as the market considers all that excess oil. One more item on price is the US Dollar (DXY) correlations. Right now there is a positive 0.73 correlation with the DXY. The DXY is in a bearish (downward bias) trend. As long as the USD Index stays bearish, it should act as a bit of a headwind for the price of oil.